Credit cards create time, not cash.

For an Amazon reseller, inventory must arrive, get prepped, check in, sell, and reach a payout. A card with a purchase grace period may let you hold cash longer while that cycle runs.

The strategy is to understand each card's statement closing date, schedule purchases near the start of a new billing cycle, record the plan in 3P Mercury, and pay according to the card agreement.

Credit is a timing tool, not permission to overspend.

How Statement Timing Creates Working Capital

A card's billing cycle has a closing date. Purchases posted after that date generally appear on the next statement rather than the statement that just closed.

If the card offers a grace period on purchases and you remain eligible for it, paying the full statement balance by the due date may prevent interest on those purchases. The Consumer Financial Protection Bureau defines a grace period as the time between the end of a billing cycle and the payment due date. Not every card must offer one.

A purchase posted just before statement close may be due relatively soon. One posted just after closing may receive nearly a full billing cycle plus the period before payment is due.

What Regulation Z means here

Regulation Z is a federal rule that gives consumer credit cards certain disclosures and payment protections. Consumer-card issuers, for example, generally must deliver statements at least 21 days before payment is due.

Business-purpose cards are exempt from most Regulation Z requirements. Do not assume a business card provides the same statement timing, grace period, or billing-dispute process as a personal card. Similar terms may appear in the card agreement, but verify them for that account.

Example with staggered closing dates

These are planning examples, not promised card terms.

| Card | Statement closes | Planned purchase | Example due date | Approximate time |

|---|---|---|---|---|

| Card A | May 1 | May 2 | June 25 | 54 days |

| Card B | May 8 | May 9 | July 1 | 53 days |

| Card C | May 15 | May 16 | July 8 | 53 days |

| Card D | May 22 | May 23 | July 15 | 53 days |

Staggered dates may create a fresh billing cycle roughly every week. They do not guarantee inventory will sell before payment is due.

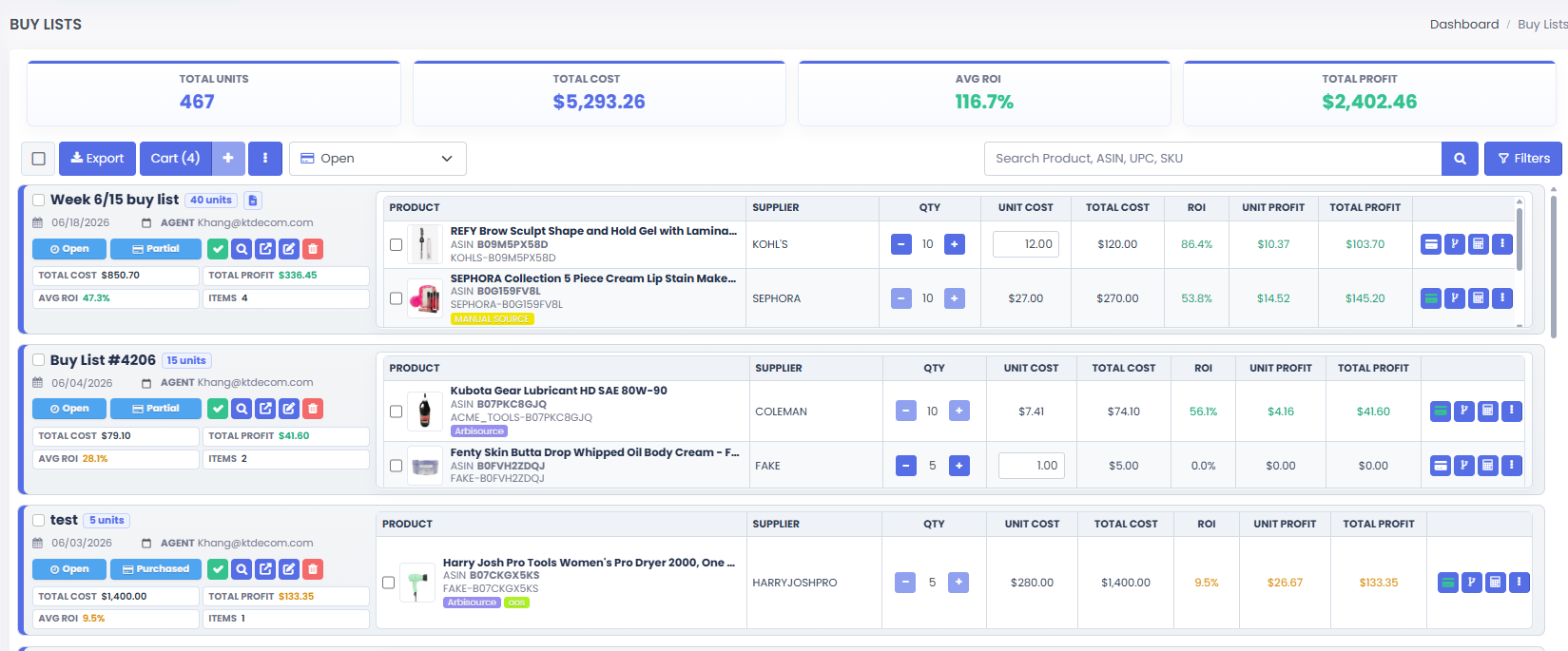

Plan Spending in 3P Mercury Buy Lists

Knowing the dates is only half the job. You must still control what to buy, the spending limit, and which card funds it.

3P Mercury Buy Lists turn a card calendar into a purchasing plan. Group the products and review total units, total cost, expected ROI, and expected profit before anyone charges a card.

Then use the desired purchase date and notes to record:

- Planned purchase date

- Card nickname or last four digits

- Statement closing date

- Payment due date or promotional payoff date

- Maximum approved spend for that buying window

- Supplier promotion or order deadline

If Card B closes on the 8th, set the desired purchase date for the 9th and add a note such as: "Use Card B ending 1234. Payment due July 1. Maximum order $2,500."

Now the buyer knows when to order, which card to use, and where to stop. The credit limit is not the budget. Set the budget from cash, obligations, sell-through, and repayment capacity; enforce it with the Buy List total.

For the complete purchasing workflow, read How to Purchase Inventory Effectively with 3P Mercury.

Build a Multiple-Card Purchasing Calendar

For each card, record:

- Card nickname and last four digits

- Consumer or business-purpose account

- Closing date and due date

- Purchase grace-period requirements

- Purchase APR, fees, and promotional expiration date

- Current balance and available credit

Confirm these details in the current agreement or with the issuer. Ask whether dates can be adjusted, but do not assume changes are allowed.

Place the verified dates on one calendar. Cards closing around the 1st, 8th, 15th, and 22nd could create four buying windows. Give each window a 3P Mercury Buy List, desired date, selected card, and spending cap.

Set three rules:

- Schedule automatic minimum payments as a backup.

- Keep upcoming payments visible in the cash forecast.

- Stop purchasing when cash and reserves cannot cover the card obligations.

Card rotation should never become debt rotation.

Use a 0% Introductory APR as a Growth Window

Some cards offer a 0% introductory purchase APR for a limited period, such as 12 months. This may allow more time to sell inventory and reuse the proceeds before the promotion ends.

A true 0% introductory APR is different from deferred interest. With deferred interest, missing the payoff deadline can trigger interest calculated back to the original purchase date. Monthly minimum payments are still normally required, and a late payment may end a promotion.

A five-cycle example

Assume a seller puts $5,000 of inventory on a 12-month 0% purchase APR card. The inventory cycle takes 60 days and produces a 20% net return after selling costs. The seller reinvests all recovered cash and plans to stop after month 10, leaving two months to settle the promotional balance.

| Cycle | Month completed | Buying power after sale |

|---|---|---|

| Starting purchase | 0 | $5,000 |

| Cycle 1 | 2 | $6,000 |

| Cycle 2 | 4 | $7,200 |

| Cycle 3 | 6 | $8,640 |

| Cycle 4 | 8 | $10,368 |

| Cycle 5 | 10 | $12,442 |

Here, the original $5,000 completes five cycles. After reserving $5,000 to repay the card, theoretical growth is $7,442.

That is math, not a forecast. It ignores minimum payments, taxes, refunds, overhead, delays, and uneven returns. A safer plan would:

- Verify the exact promotional end date and post-promotion APR.

- Schedule every required minimum payment.

- Target payoff one or two billing cycles before the promotion expires.

- Use proven, fast-moving replenishments rather than risky test inventory.

- Track the original card obligation separately from cash available to reinvest.

- Stop recycling early if sell-through falls behind the plan.

Possible cycles depend on actual inventory speed. A 60-day cycle may fit five times in ten months; a 90-day cycle may fit only three. Use real sales history, not optimistic projections.

Follow This Action Plan

- Map the inventory cycle: shipping, prep, receiving, sell-through, returns, and payout.

- Verify every card: account type, dates, grace period, APR, fees, and promotional deadline.

- Create buying windows on one calendar.

- Create a Buy List for each window with products, purchase date, card, due date, and maximum spend.

- Prioritize replenishments with actual sales, refund, and velocity data.

- Review weekly against payouts and reserves.

- Pay early. Never depend on a final-day payment or one ASIN selling.

For the broader operating system, read How to Manage Amazon Cash Flow Without Running Dry.

This article is educational and not individualized financial, tax, or legal advice. Credit terms and business circumstances vary. Review current agreements and consult a qualified financial professional when needed.

Frequently Asked Questions

How can credit cards increase cash flow?

They can delay when cash leaves the business. A purchase grace period or 0% promotional APR may allow inventory to move through part of its sales cycle before the balance must be fully repaid.

When should I make an inventory purchase?

A purchase posted just after statement close may receive more time before its due date. Verify the closing date, posting rules, due date, and grace-period terms, then schedule the date and selected card in a 3P Mercury Buy List.

How many times can I recycle 0% credit?

Divide the safe operating window by your actual inventory cycle. Five 60-day cycles fit into ten months, while three 90-day cycles fit into nine months. Leave time before the promotion ends to repay the balance.

What happens if I cannot pay as planned?

You may owe interest, lose promotional terms, or face fees depending on the agreement. Deferred-interest offers may also impose interest calculated from the original purchase date.

How does 3P Mercury help manage card timing?

Buy Lists show planned cost before checkout. Desired purchase dates and notes document which card to use, when to buy, when payment is due, and the spending cap for that window.

Plan Every Purchase Before the Card Is Charged

Sign up for 3P Mercury to simplify your business. The one software that takes you from sourcing to shipping, automated with the power of AI.

Sign up for 3P Mercury